Introduction

In June 2025, the U.S. Federal Reserve (Fed) announced it would maintain the federal funds rate at 4.25%–4.50%, continuing a pause first established in December 2024. This decision reflects a cautious approach amid persistent inflation, robust job growth, and future economic uncertainty

For readers of Manika FinTax Solutions, this article explores how these rate decisions shape your finances—from loans and savings to investment planning.

What’s the Federal Funds Rate and Why It Matters

The federal funds rate is the benchmark interest rate at which banks lend to each other overnight. Set by the Fed, it influences a wide range of financial products—mortgages, car loans, credit cards, and savings rates .

Why it matters:

-

Borrowers: Higher rates mean costlier loans.

-

Savers: Higher yields on deposit accounts.

-

Economy: It's the Fed's main weapon to control inflation and support jobs.

Recent Fed Decision: Maintain, But Prepare for Cuts

At its June 18 meeting, the Fed:

-

Held the rate steady at 4.25%–4.50%, its sixth straight unchanged decision

-

Indicated two potential 25 bps rate cuts later this year, targeting around 3.75%–4.00% by year-end

-

Revised forecasts: inflation expected at 3.0%, unemployment rising to 4.5%, GDP growth slowing to 1.4%

-

Chair Powell emphasized a data-dependent strategy—balancing inflation risk and labor market resilience

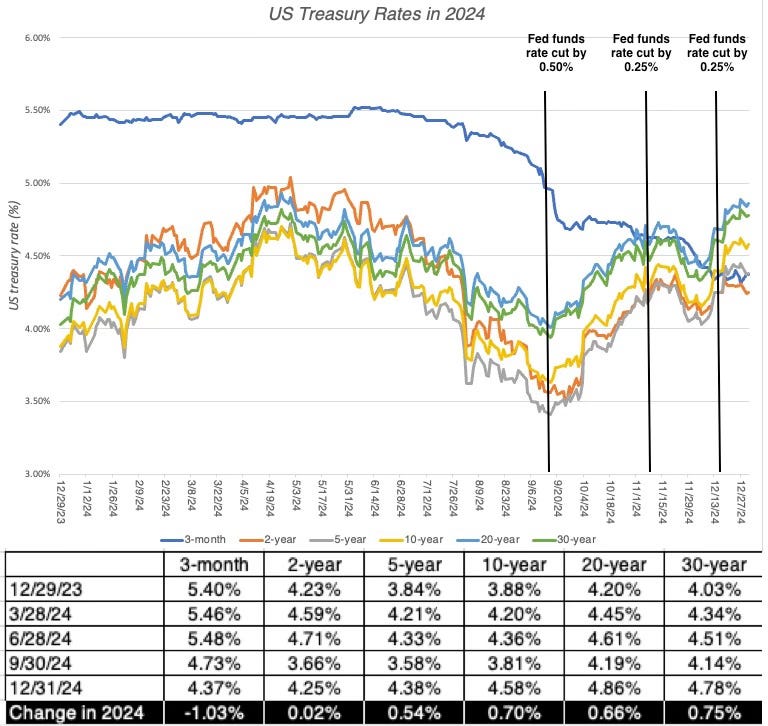

Quick Facts – Federal Funds Rate Timeline

| Date | Fed Funds Rate | Notes |

|---|---|---|

| Dec 18, 2024 | 4.25%–4.50% | Rate first held steady |

| Jun 18, 2025 | 4.25%–4.50% | Continued pause; future cuts signaled |

| May 2025 (avg.) | 4.33% | Effective federal funds rate |

Why the Fed Is Holding Off on Cuts

Analysts cite four main reasons

-

Inflation remains elevated—core inflation around 3%, above the Fed's 2% target .

-

Tariffs pose upside inflation risks, especially from trade tensions

-

Labour market remains strong—unemployment near 4.2% with solid job creation

-

Forward‑looking caution—avoiding premature rate cuts while inflation uncertainties persist investopedia.com.

Impact on Everyday Finances

1. Borrowing Costs

-

Mortgages & auto loans: Rates follow the Fed trend—remain elevated.

-

Example: A ₹20 lakh home loan at 7% vs. 6%—monthly EMI difference ~₹2,500.

2. Savings & Deposits

-

Higher interest rates mean better returns on fixed deposits (FDs) and savings accounts.

-

Tip: Shop around for best FD rates; consider locking in 1-year FDs at ~7%+.

3. Investment Outlook

-

Stocks: Prosper in lower-rate environments; future cuts may boost markets

-

Bonds: Prices fall in high-rate scenarios; as cuts arrive, bond prices rebound.

4. Small Businesses

-

Business loans pricier now; plan capital expansions when cuts materialize.

Practical Tips for Manika FinTax Readers

✔️ Review your debt portfolio:

Refinance if nearing repayment windows—future cuts may lower rates.

✔️ Fix your savings yields:

Avoid locking long-term if cuts are anticipated later in the year.

✔️ Diversify investments:

Blend equities with bond funds to ride both rate scenarios.

✔️ Monitor economic data:

Reserve rate moves hinge on inflation/job data—stay informed.

Forecast Ahead: What’s Next for 2025?

-

Two quarter-point rate cuts predicted—bringing core rate to ~3.75%–4%.

-

Data-dependent path means cuts only with healthy inflation drop and subdued job market

-

Risks remain—tariffs, geopolitical fallout, and sticky inflation (runway to stagflation) could delay easing .

Conclusion

The Fed's steady stance reflects a cautious balance: curbing inflation without undermining economic growth. For savers, this means good returns—while borrowers face elevated costs, with hope on the horizon for rate cuts.

Key takeaways:

-

Borrowing remains expensive, but savings shine.

-

Watch inflation and job data—they guide the Fed's timing.

-

Expect gradual easing later this year, not immediate relief.

Frequently Asked Questions (FAQs)

Q1. When will the Fed cut rates?

Fed officials signal two cuts in 2025, but dates depend on inflation and employment trends.

Q2. How do rate decisions affect my loan?

Loan rates adjust with Fed policy; fixed loans remain constant, while variable loans fluctuate.

Q3. Are savers better off now?

Yes—higher rates benefit fixed deposits, savings accounts, and short-term debt instruments.

Q4. What is “data‑dependence”?

Meaning the Fed waits for clear trends in inflation and job market before changing rates.

Q5. Should I refinance now or wait?

If your loan is about to renew, consider refinancing after cuts arrive to benefit from lower rates.

Call to Action

Have questions on how these interest rate shifts affect your tax or finance strategies? Reach out to Manika FinTax Solutions for personalized advice and paid filing support! 🚀

Recent Fed News & Analysis:

US Fed keeps rates steady, sees 50 bps rate cut in 2025

Fed's Latest Economic Projections Hint at Stagflation Concerns

4 Reasons The Fed Isn't Cutting Interest Rates

Post a Comment

0Comments